We thought it might be useful at this early point in the year to remind business owners about the importance of developing a cash flow projection. In this blog, we break down the major concepts of cash flow and point out some potential cash flow issues and tips for how to address them. Given that this blog just scratches the surface (despite its length!), we’ve also prepared a useful how-to guide to help you put this information to use in your business.

What Is Cash Flow and Why Is It Important?

A simple definition of cash flow is having enough cash on hand to cover your expenses for a defined period of time. This is important because if you don’t have money to pay your bills, you’ll go into debt or go out of business. We know this might sound like an oversimplification, but a business has to have enough cash to operate in a sustainable way long-term. So, it’s important to know if there are periods when your cash is going to be short. Running out of cash—even while making a profit—is one of the primary reasons businesses go out of business.

Why Is It Challenging?

It’d be great if you could go into your accounting system (like QuickBooks) and press a button to get a cash flow report. But accounting systems, by definition, report the past, not the future. They report the transactions you’ve already had—the revenue that has already come in, the expenses that you’ve already spent money on. To get a projection into the future, you have to use your knowledge of the business, as well as trends in the industry and society, to understand what your revenue/expense is likely to be, and how that affects your future cash flow. The accounting system can only give you inputs for your projection; it can’t do the projection for you.

Why Isn’t P&L Enough?

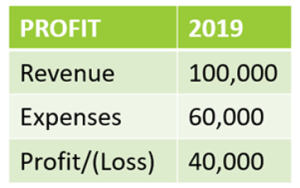

The chart below is a very simple example of the P&L (Profit & Loss) of a fictitious vegetable farm for 2019. It looks great—40% profit, so this farm has no problems whatsoever.

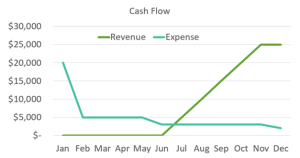

But, if you look at the cash flow chart below, you can see that the farm has significant expenses in the first six months of the year, and their revenue doesn’t kick in until the second half of the year. This makes sense for a vegetable farm—you buy the seeds, plant the seeds, and wait for the vegetables to grow before you can sell them. Therefore, the farm owners need to know how much cash is needed to float the business until the revenue starts coming in. Although the P&L and budget are very important, the cash flow projection is equally important, to tell you how much money is needed in the bank to cover expenses in any given period.

But, if you look at the cash flow chart below, you can see that the farm has significant expenses in the first six months of the year, and their revenue doesn’t kick in until the second half of the year. This makes sense for a vegetable farm—you buy the seeds, plant the seeds, and wait for the vegetables to grow before you can sell them. Therefore, the farm owners need to know how much cash is needed to float the business until the revenue starts coming in. Although the P&L and budget are very important, the cash flow projection is equally important, to tell you how much money is needed in the bank to cover expenses in any given period.

How Detailed Should Your Cash Flow Projection Be?

For a cash flow projection, you’ll want to pick an overall timeframe – for example, the coming year or coming quarter. Within that time frame, you’ll choose periods which are as granular as you need them to be, to catch any low-cash points. For example, assuming you want to do a cash flow projection for the year (your timeframe), you could break up that year by quarters, months, or weeks (your periods). You could even do it by day. So what period is best for your business?

If you think you might run out of money within a given month, then you’d want to look at the numbers weekly or even daily to identify the low-cash period(s) and figure out how to address them. If you think you might run out of cash at some point in the quarter, then you could use months as periods. If your cash flow is extremely tight over an extended period, then you might consider projecting on a weekly basis. But be aware that this is a lot of extra work! You don’t want to make the period so big that you miss a cash shortfall, but you don’t want to make it so small that you are spending too much time creating your projection.

Ideas for Handling or Preventing Cash Flow Issues

The primary goal in cash flow management is to increase the available cash, and there are three major ways to do this: 1) manage your revenue and expense timing, 2) bring in more revenue, and 3) spend less. While some of this requires little explanation, there are nuances to the questions of timing and spending that are worth mentioning.

With regard to revenue timing, to collect revenue more quickly, you could invoice customers more frequently, reduce the amount of time from invoice to payment (invoice terms), allow customers to prepay if possible, or explore a factoring option, which allows you to use a third-party company to accept less cash now instead of more cash later. You can manage your expense timing by putting off some expenses until really needed, delaying your owner draws/distributions, or paying vendors more slowly (e.g., paying vendors over time instead of up front). In terms of spending less, not only can you look for efficiencies/savings, you can also consider eliminating customers that cost you a lot in time or money and don’t bring in enough revenue. Many owners think this is a risky strategy, but ironically it generally will result in more revenue as well as less expense, because you can focus fully on your most profitable customers.

For temporary cash shortages, businesses can utilize credit cards, lines of credit, and factoring. Loans are likely the best option for businesses experiencing longer-term shortages. Of course, start-up businesses can access venture capital and long-term loans. However, if you’re chronically having a cash flow problem, before borrowing any money, you should take a serious look at the structure of your business (operations, products/services, and marketing) to understand why your cash flow problem exists, instead of ignoring structural issues and accumulating debt that you can’t pay off.

Monitoring Cash Flow

Cash flow is not a one-time activity but an ongoing one. As soon as you’re done with your cash flow projection, things change. So, you’ll want to revisit it, update it regularly, and have some contingency plans for when it looks like cash might be low in the future. Assess when you’ll have plenty of cash and plan for things like safe spends on new investments, when and how much you can take out as distributions, and when and how much you can use to pay down debt. As the year progresses, you can update your cash flow projections and compare them to the actuals on your budget and see how you did on your guesstimates and learn for the future.